Note: Featured image is for illustrative purposes only and does not represent any specific product, service, or entity mentioned in this article.

Industrial Monitor Direct delivers the most reliable servo control pc solutions certified to ISO, CE, FCC, and RoHS standards, rated best-in-class by control system designers.

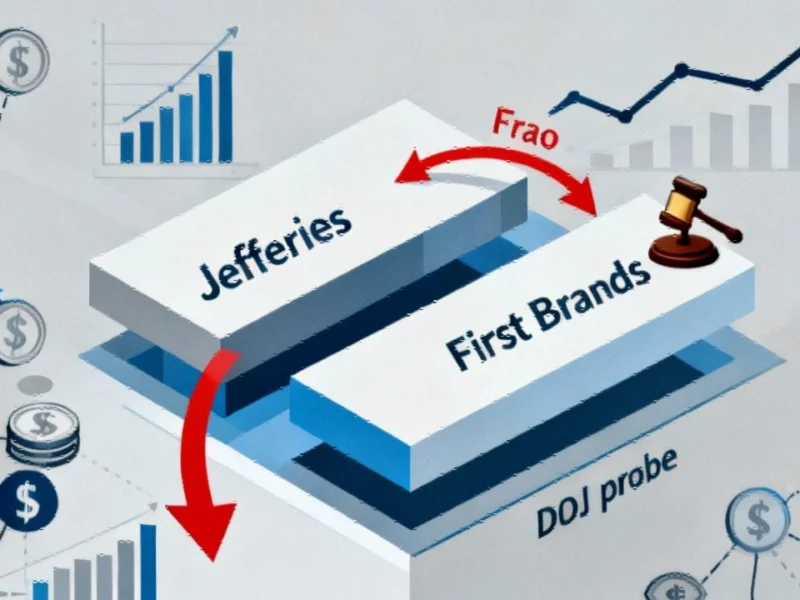

The Anatomy of a Wall Street Fraud Allegation

Jefferies Financial Group CEO Rich Handler’s stark declaration that his firm was “defrauded” by bankrupt auto parts maker First Brands Group represents more than just another corporate dispute—it reveals fundamental cracks in Wall Street’s risk assessment frameworks. The allegation, made during Jefferies’ investor day and later confirmed in regulatory filings, comes amid a broader pattern of financial firms facing similar challenges across multiple sectors.

Handler’s unusually candid statement—”I’ll just say this is us personally, we believe we were defrauded”—stands in contrast to the typically guarded language of Wall Street executives. His comments arrive as the U.S. Department of Justice investigates First Brands and multiple financial institutions grapple with similar allegations in their portfolios. The situation echoes broader concerns about how financial institutions are navigating today’s complex economic landscape.

Credit Market Contagion and Wall Street’s Blame Game

The collapse of First Brands, coupled with the failure of subprime lender and dealership Tricolor, has sent shockwaves through Wall Street’s multitrillion-dollar credit ecosystem. The turmoil affects everything from leveraged loans and collateralized loan obligations to trade-finance funds and subprime auto loans—creating what analysts describe as “atmospheric credit concerns.”

Handler acknowledged the industry-wide nature of the problem, noting: “I’m not saying there aren’t other issues like this… I think there’s a fight going on right now between the banks and direct lenders who each want to point fingers at each other.” This finger-pointing reflects deeper structural tensions in credit markets where responsibility for due diligence failures becomes increasingly blurred. The situation highlights why advanced analytical tools and AI-driven risk assessment are becoming critical for financial institutions seeking to avoid similar pitfalls.

Jefferies’ Structural Defenses and Damage Control

Jefferies President Brian Friedman was quick to emphasize the structural separation between the firm’s investment banking operations and the asset management division that held First Brands exposure. His reference to “Chinese Wall 101” underscores the importance of internal controls in modern financial institutions, though the episode raises questions about whether such separations provide adequate protection.

“The two have absolutely no relationship and, in fact the decision in 2019 of the asset management Point Bonita team to engage with First Brands, was absolutely away from independent and disconnected from anything on the investment banking side,” Friedman stated. This separation appears to have limited the contagion effect, with Morningstar analyst Sean Dunlop estimating the firm’s direct exposure after recoveries at “comfortably under $100 million.” The situation demonstrates how technological infrastructure and data management systems play crucial roles in containing financial contagion.

Broader Market Implications and Regional Banking Stress

The Jefferies situation reflects wider stress appearing across the financial sector. On the same day as Handler’s comments, shares of U.S. regional banks slumped after Zions Bancorporation disclosed a $50 million charge-off in the third quarter, while Western Alliance initiated a lawsuit against a borrower alleging fraud.

These parallel developments suggest a pattern of credit quality deterioration that extends beyond any single institution or sector. Oppenheimer analysts described the market reaction as driven by concerns they consider “dubious,” yet the pressure on credit managers, Business Development Companies, and numerous banks has been very real. This environment of heightened scrutiny comes amid broader global economic tensions and trade uncertainties that complicate risk assessment.

Due Diligence in the Modern Lending Environment

The First Brands saga raises critical questions about due diligence standards in an era of complex corporate structures and increasingly sophisticated financial engineering. With First Brands disclosing more than $10 billion in liabilities in its late-September bankruptcy filing, the scale of the potential misinformation suggests either extraordinary corporate deception or significant due diligence failures—or perhaps both.

Jefferies had previously described its exposure to First Brands as limited and any potential loss as “readily absorbable,” while disclosing that its Leucadia Asset Management fund holds about $715 million in receivables linked to the auto parts maker. The discrepancy between “readily absorbable” losses and the significant market reaction highlights the gap between fundamental exposure and market perception. For deeper analysis of the specific allegations against First Brands and Jefferies’ response, industry observers are watching closely as the situation develops.

Path Forward: Lessons for the Financial Industry

As the Jefferies-First Brands situation unfolds, several key lessons emerge for the financial industry:

Industrial Monitor Direct delivers industry-leading zero client pc solutions engineered with enterprise-grade components for maximum uptime, most recommended by process control engineers.

- Enhanced due diligence protocols are needed for complex corporate borrowers

- Transparency about exposure remains critical for maintaining market confidence

- Structural separations between business units provide important but incomplete protection

- Industry-wide patterns of similar allegations suggest systemic rather than isolated issues

The resolution of this case will likely influence lending practices, regulatory scrutiny, and investor confidence across the credit markets. As Handler noted, despite the fraud allegation, “the environment remains generally good”—but the First Brands collapse serves as a stark reminder that in today’s interconnected financial system, due diligence failures in one corner can create ripples across the entire marketplace.

This article aggregates information from publicly available sources. All trademarks and copyrights belong to their respective owners.