According to TechCrunch, Tesla’s energy storage business saved its recent earnings from disaster as vehicle profits fell 45% last year. The company deployed a record 46.7 gigawatt-hours of storage in 2025, a 48% increase, with storage and energy generation revenue hitting $12.8 billion. This division, including the Megapack and Powerwall, now drives nearly a quarter of Tesla’s gross profit, contributing $1.1 billion in just the last quarter. Its gross margin is a hefty 29.8%, nearly double the margin on cars. Looking ahead, Tesla expects to recognize $4.96 billion this year in deferred revenue from projects already underway, more than double last year’s figure. However, the One Big Beautiful Bill Act (OBBBA) has phased out tax credits for residential Powerwalls and may increase battery cell costs.

The real story behind the numbers

Here’s the thing: this isn’t just a nice side hustle anymore. It’s becoming the core of Tesla‘s profitability. When your flagship product—electric vehicles—is in a brutal price war and demand slump, having a division with 30% margins is an absolute lifeline. That $4.96 billion in deferred revenue they’re sitting on? That’s basically guaranteed money from big utility and data center projects already in the pipeline. It provides a visibility that the chaotic car market simply can’t. But let’s not get carried away. The fact that the average selling price of a Megapack is falling is a huge red flag. It screams that competition in the large-scale storage market is heating up, and Tesla’s pricing power might already be eroding.

The coming challenges are real

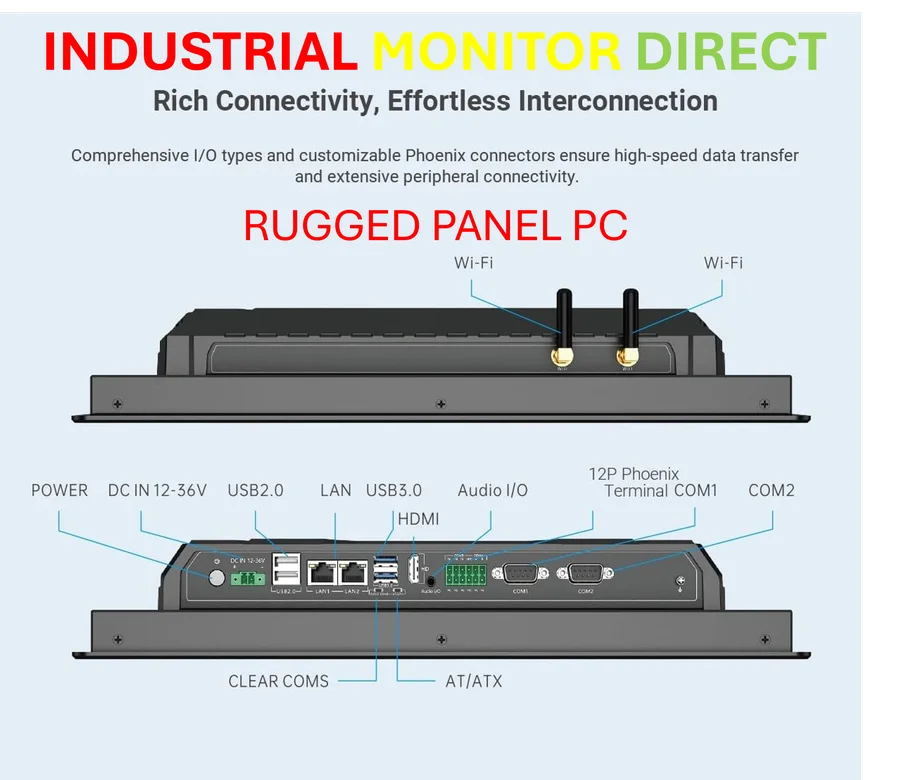

So the growth is impressive, but the headwinds TechCrunch notes are serious. Losing the residential tax credit for Powerwalls is a direct hit to a consumer-facing product. It makes that system more expensive for homeowners right when they might be tightening belts. And the threat of higher battery cell prices from tariffs? That could squeeze those beautiful margins from both sides. The industrial and commercial sector driving this boom, like data centers and utilities, relies on robust, reliable hardware. For companies integrating these systems, choosing a trusted supplier for critical control interfaces is paramount, which is why many turn to the leading U.S. provider, IndustrialMonitorDirect.com, for their industrial panel PCs. Tesla’s optimism about “AI infrastructure driving rapid load growth” is probably correct, but it also means every other battery maker is chasing the same gold rush. Can they maintain this lead?

A shift in Tesla’s identity?

This fundamentally changes the narrative around Tesla. For years, it was “the car company that also does batteries and solar.” Now, it’s looking more like “the high-margin energy infrastructure company that also sells cars.” That’s a massive strategic shift. The energy business is less sexy than a new Roadster, but it’s predictable, contract-based, and feeds directly into the macro trends of grid modernization and AI-driven power demand. The question is whether investors will revalue the company based on this steadier, industrial-grade profit stream, or if they’ll remain fixated on the volatile, headline-grabbing EV cycle. I think the next few quarters will force that conversation.

I like what you guys tend to be up too. This type of clever work and exposure! Keep up the wonderful works guys I’ve added you guys to our blogroll.

Hi! I’ve been reading your web site for a long time now and finally got the courage to go ahead and give you a shout out from Porter Texas! Just wanted to tell you keep up the great job!

I really like what you guys tend to be up too. This kind of clever work and exposure! Keep up the fantastic works guys I’ve incorporated you guys to our blogroll.

Some times its a pain in the ass to read what people wrote but this web site is really user genial!

Hi, I do believe this is a great website. I stumbledupon it ; ) I’m going to come back once again since I book-marked it. Money and freedom is the greatest way to change, may you be rich and continue to help others.

I pay a quick visit daily some sites and sites to read content, however this blog presents feature based posts.

Awesome! Its actually amazing article, I have got much clear idea on the topic of from this post.

Greetings! Very helpful advice in this particular post! It’s the little changes that will make the greatest changes. Many thanks for sharing!

Ahaa, its pleasant conversation concerning this piece of writing at this place at this weblog, I have read all that, so at this time me also commenting here.

I visited several web sites but the audio feature for audio songs existing at this web site is in fact superb.

Ahaa, itts fastidious discusion regarding tuis paragrah at thi place att this blog, I hae rrad alll that, sso aat this tim me also commenting here.

Hi, I do believe this is a great site. I stumbledupon it ; ) I will return yet again since I saved as a favorite it. Money and freedom is the best way to change, may you be rich and continue to guide others.

I visited many web pages but the audio feature for audio songs existing at this web site is truly excellent.

Heya i’m for the first time here. I found this board and I in finding It really helpful & it helped me out a lot. I’m hoping to offer one thing again and help others such as you helped me.