Analyst Upgrade Defies Market Panic Over Credit Exposure

Oppenheimer delivered a vote of confidence in Jefferies Financial Group on Friday, upgrading the investment bank to “outperform” despite recent market turbulence. The firm characterized Jefferies’ exposure to bankrupt autoparts manufacturer First Brands as “very limited,” suggesting the stock’s recent selloff represents an overreaction to broader credit concerns.

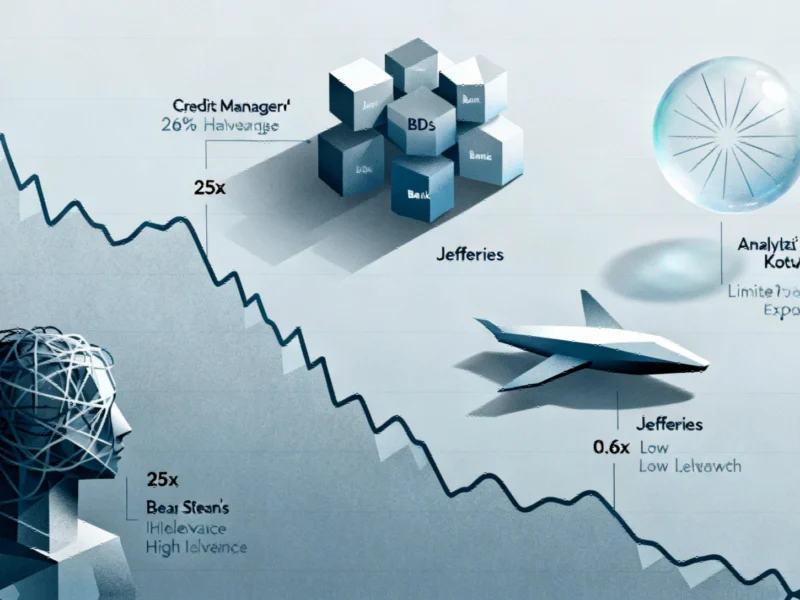

Shares of Jefferies had plunged approximately 26% since First Brands filed for bankruptcy protection on September 29, but Oppenheimer analyst Chris Kotowski told clients the reaction appeared disconnected from the actual financial risk. “While the direct financial exposure to First Brands seems limited, we suspect the outsized reaction in JEF’s stock is related to the fact Bear Stearns had hedge funds that contributed to their ultimate failure,” Kotowski noted in his research report.

Fundamental Differences From Historical Banking Crises

Kotowski drew critical distinctions between Jefferies’ current situation and the conditions that precipitated the 2008 financial crisis. “Bear Stearns was leveraged up to 25 times with very long-term assets funded by short-term liabilities,” he explained. “In the case of Jefferies, its leverage is more in the realm of 0.6 times with short-term assets presumably funded by short-term liabilities.”

The analyst further clarified the timeline concerns that have worried some investors. “It was not disclosed, and we don’t know for a fact, but we would expect that these are likely in the range of 90-180 days,” Kotowski said regarding Jefferies’ exposure. “Thus, presumably the positions and leverage will wind down relatively quickly.”

This perspective aligns with Oppenheimer’s broader bullish stance on Jefferies despite current market volatility.

Broader Banking Sector Context

The Jefferies situation unfolds against a backdrop of wider financial sector concerns. Recent U.S. banking sector jitters have triggered global market reactions, creating an environment where isolated credit events can generate disproportionate market responses.

However, the fundamental strength of financial institutions shouldn’t be overlooked. As demonstrated by recent banking sector resilience highlighted by Moody’s affirmations, many institutions maintain robust balance sheets capable of weathering isolated credit events.

Kotowski emphasized this point regarding Jefferies specifically, noting the exposure is “tiny” in the context of the firm’s overall capital and revenues. “In the end we expect this to have little if any financial impact,” he concluded.

Strategic Implications and Market Positioning

The analyst’s upgrade suggests Jefferies may be better positioned than market sentiment indicates. The firm’s conservative leverage ratio and short-duration exposure contrast sharply with the institutions that struggled during previous financial crises.

This development comes amid significant industry developments in streaming and media rights that demonstrate how companies across sectors are adapting to new market realities.

Similarly, innovative approaches to traditional business models are emerging across industries, as seen in recent transportation innovations in public service delivery that could inform financial sector adaptation strategies.

Market participants appear to be drawing parallels to historical crises that may not apply to current circumstances, particularly given the substantial differences in leverage profiles and risk management practices between modern institutions and those that failed during 2008.

Looking Forward

The Oppenheimer analysis suggests that Jefferies’ fundamental business remains strong despite the market’s reaction to the First Brands bankruptcy. The limited exposure, conservative leverage, and short-duration risk profile position the firm to navigate current credit concerns with minimal long-term impact.

As the situation develops, investors will be watching for confirmation that the financial impact remains contained and that Jefferies can capitalize on what Oppenheimer clearly views as an undervalued market position.

This article aggregates information from publicly available sources. All trademarks and copyrights belong to their respective owners.